Solana’s Dollar: Building the Future of Money on a Parallel Track

Regulations, Innovations, and Why Everyone is Paying Attention

Stablecoins are the most successful product in all of crypto, and Solana is now the best place to use them.

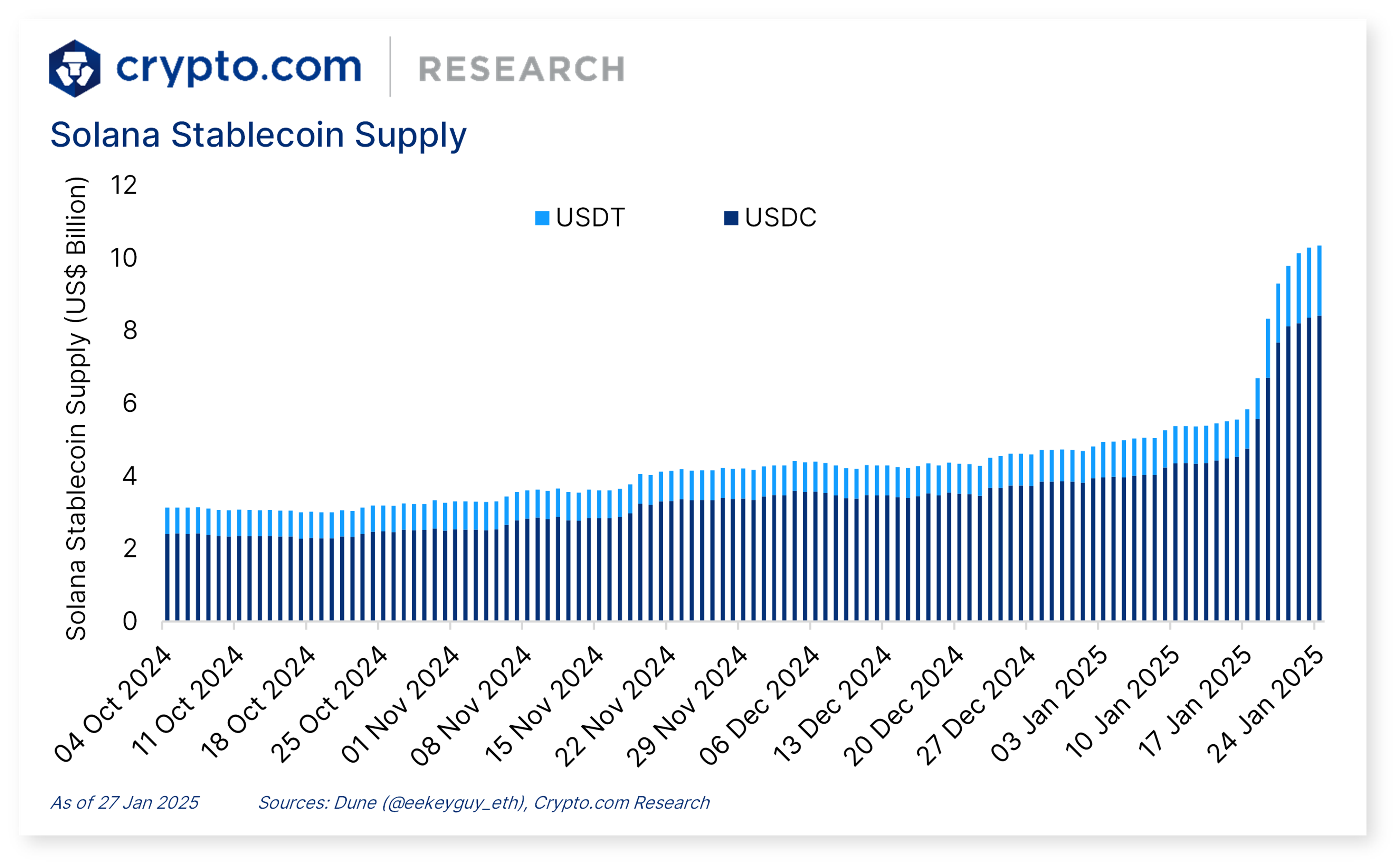

$10B - That’s the stablecoin market cap on Solana today, more than double what it was just three months ago. At its March peak, it even crossed $13B.

But this wasn’t driven by institutional inflows or major corporate integrations. The biggest surge in recent memory? It came from memecoins - $TRUMP and $MELANIA.

To understand whether this growth is meaningful or just mania, we need to dig into the numbers and follow the money.

This essay takes a closer look at the current state of stablecoins on Solana beyond the headlines and hype. I’ll unpack the key network trends, highlight the most important product developments, map out the ecosystem, and compare global regulatory movements. Along the way, I’ll explore where the real opportunities lie and why stablecoins might be Solana’s most important building block.

Stablecoins by the Numbers

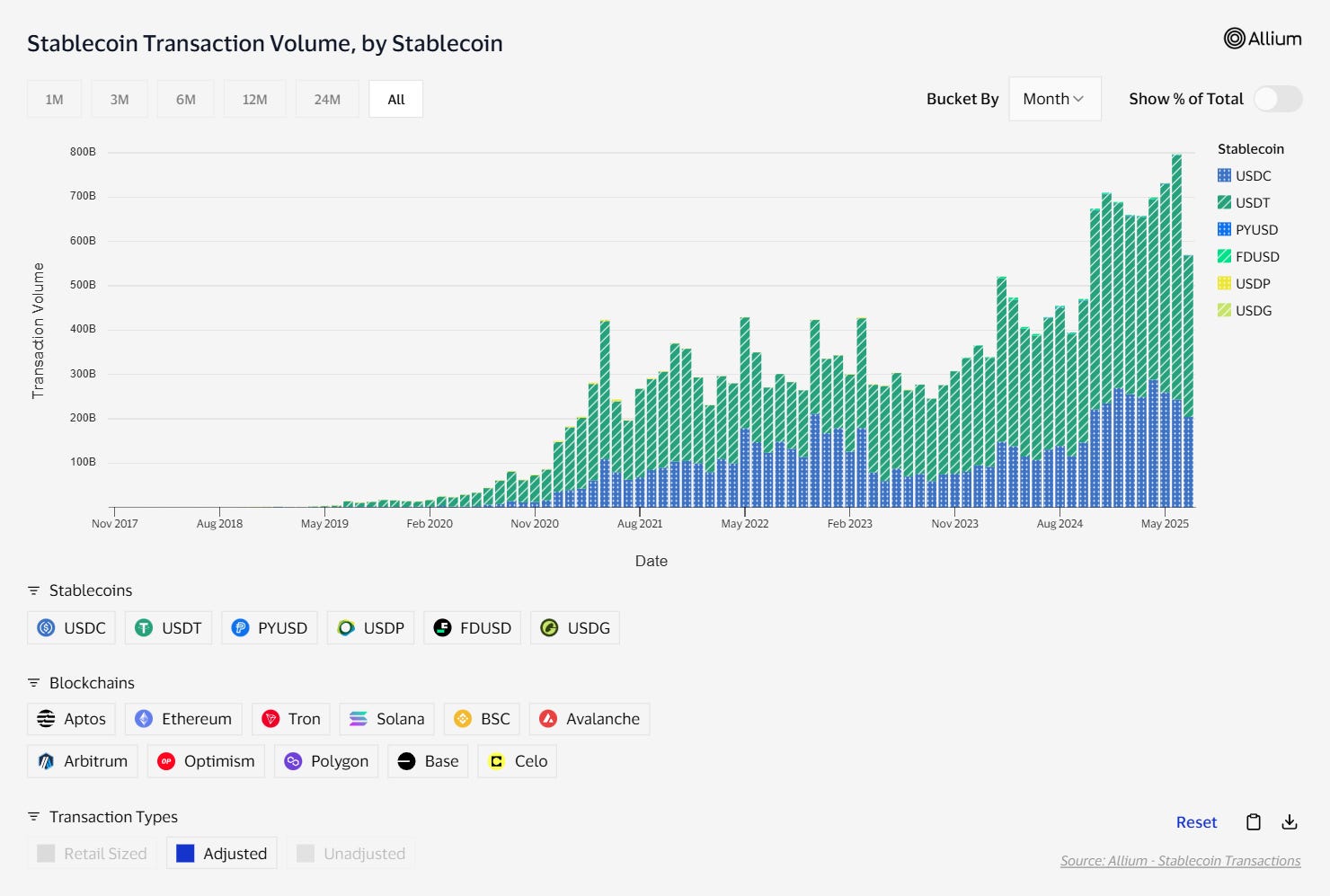

Since 2019, stablecoins have processed more than $253.7 trillion in on-chain volume across all blockchains. But when adjusted for inorganic activity, like bots, internal exchange shuffling, and smart contract noise the number compresses to $21.3 trillion, still an enormous figure. Similarly, while the total transaction count exceeds 15.2 billion, the adjusted count sits at 4.1 billion, reflecting real-world, user-driven flows.

This delta between raw and adjusted numbers reveals a core truth: blockchains are noisy, but stablecoins are signal-rich. Even when filtered conservatively, they account for trillions in real utility, whether for payments, remittances, DeFi, or on-chain commerce.

“If stablecoins on Solana were just about TVL or market cap, the story would be shallow. But dig into the data, and a deeper trend emerges: people are using them often, and at growing scale.”

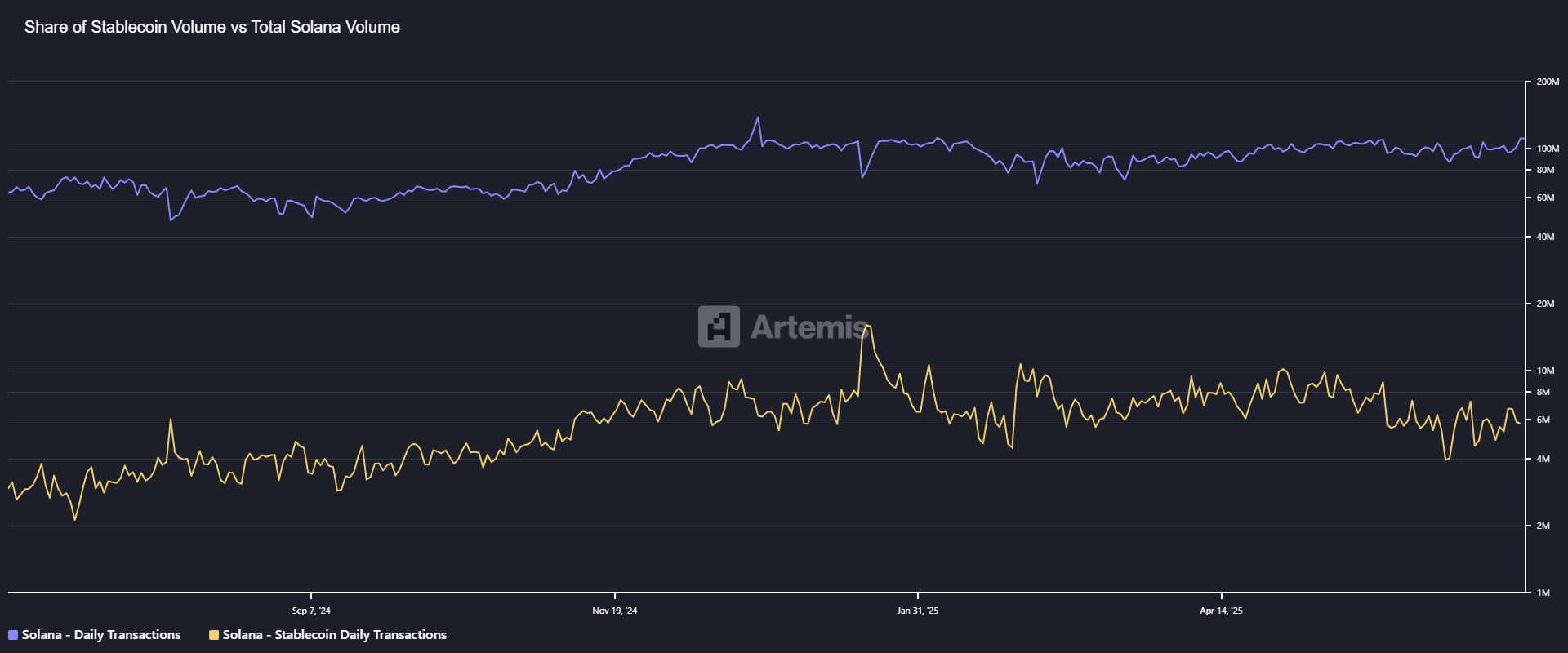

Earlier, I mentioned the $10B market cap figure, but market cap doesn’t equal utility. The real signal comes from usage. In March, Solana processed over $40B in stablecoin volume through 200M+ transactions, meaning stablecoins were moved, spent, or deployed, not just held. That’s a strong indicator of active economic behavior, not just speculative hoarding.

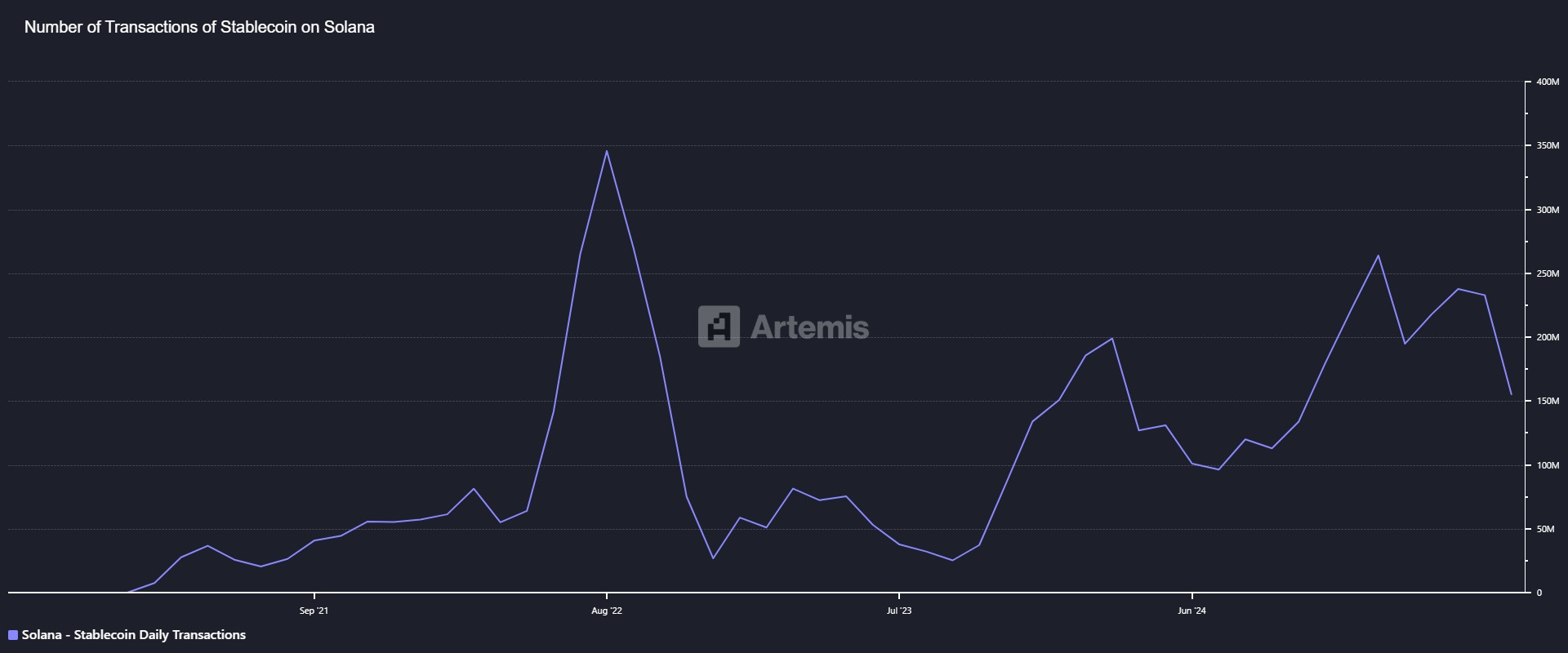

Stablecoin transaction activity on Solana has been anything but flat. After a steep surge in mid-2022 reaching nearly 350 million monthly transactions, the network saw a significant cooldown. But since late 2023, growth has returned with conviction. In early 2025, monthly transactions consistently surpassed 200 million, with a peak around March aligning with the memecoin-fueled stablecoin spike.

March may have marked a peak, but the volume hasn’t vanished. Stablecoin transactions have remained strong and steady since. Stablecoins on Solana are seeing sustained, high-frequency usage, hinting at growing adoption across both consumer and DeFi layers.

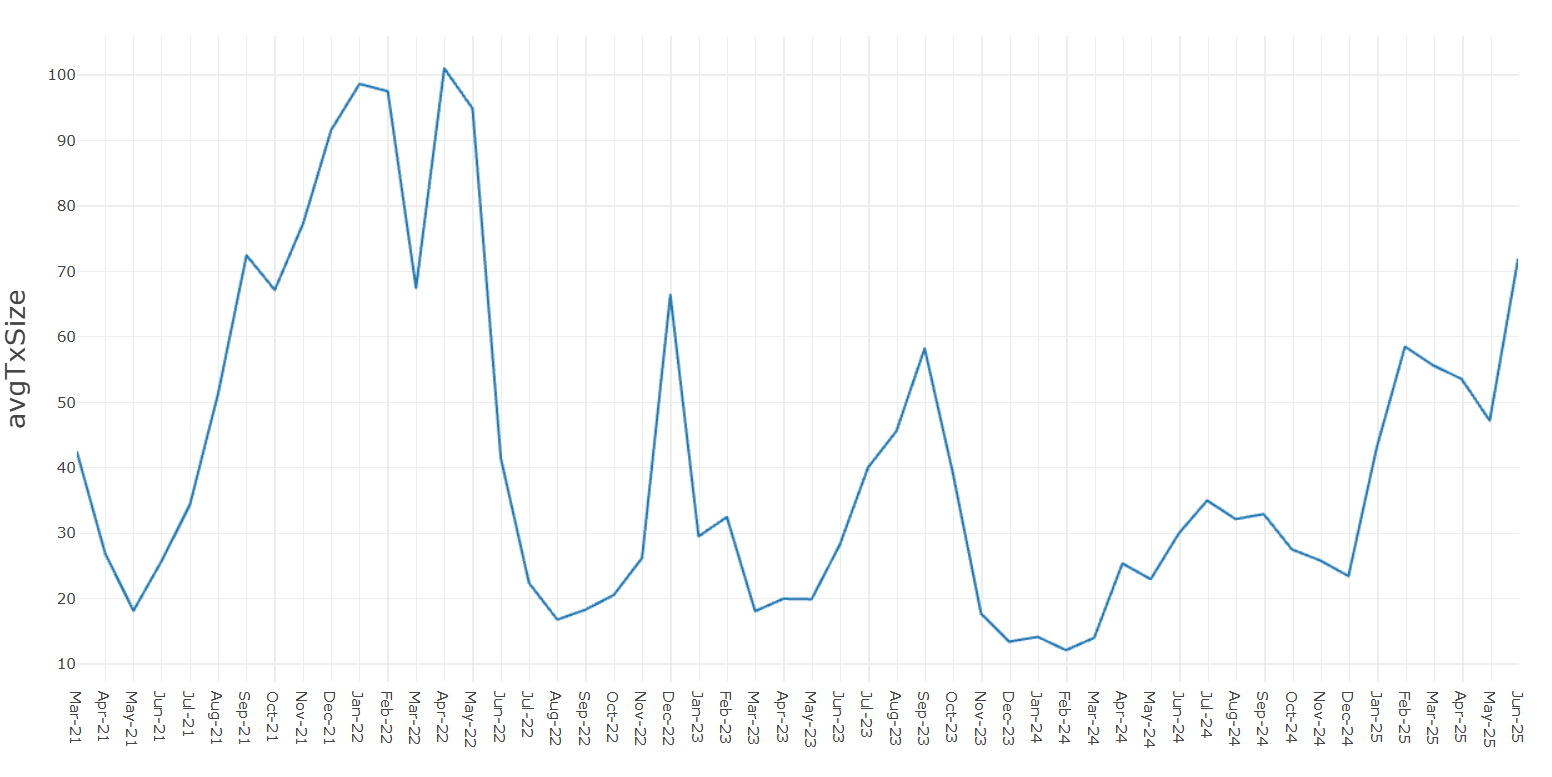

While the number of stablecoin transactions on Solana has surged in 2025, the average transaction size has risen with it significantly. After falling to under $20 in 2023, the average transaction now sits above $70. That’s more than 3x growth in just six months.

This shift matters. Smaller transactions typically signal retail usage payments, micro-transfers, or gaming. But the rising average size suggests a return of larger economic activity: perhaps payroll, institutional DeFi, or high-volume commerce. The fact that both transaction count and value are rising in parallel points to healthy, multidimensional growth, not just bots or airdrop farmers gaming metrics.

While Solana hosts everything from NFTs to memecoins, stablecoins now account for a reliable 10–15% of all daily transactions on the network. That may sound small at first glance, but for an asset class that was once barely noticeable in Solana’s activity map, this consistency signals something bigger: stablecoins aren’t just riding the wave, they’re becoming structural to Solana’s economy.

Notably, this share has held steady even as overall network volume fluctuated, meaning stablecoin usage is becoming less cyclical and more baseline. Whether it’s payroll, yield strategies, or payments, stablecoins are clearly cementing themselves as Solana’s financial backbone.

These numbers paint a clear picture: stablecoins aren’t just growing on Solana, they’re becoming a core part of how the network is actually used. But metrics alone don’t explain everything. To understand where this growth is coming from, we need to look at the apps, integrations, and products driving it.

Products & Ecosystem

Most of the stablecoin growth on Solana isn’t coming from protocols you've never heard of, it’s coming from actual product use. And not just “another DeFi primitive.” We're talking real tools: apps that pay people, move money, manage treasuries, stream wages. Some are startups, some are integrations from giants. Together, they’re turning stablecoins from a speculative asset into a functional financial layer. This section breaks down what’s being built and what actually matters.

Consumer & Infra Integrations

Think about how international phone calls used to work. Calling abroad meant burning through dollars by the minute, with clunky connections and unpredictable quality. Then the whatsapp changed everything, voice calls became fast, seamless, and free. Payments haven’t caught up. They’re still stuck in the old world: slow, expensive, and walled off by national borders and corporate toll booths.

Imagine working with two clients. One pays you through a bank. Slow, expensive, and sometimes the transfer fails. The other pays you instantly, directly to your wallet, with zero middlemen and zero hidden costs. Which one would you choose?

That’s what Stripe is doing by using Solana USDC payouts. It’s fast, cheap, and actually usable, not just some crypto fantasy.

“With transaction speeds increasing and costs coming down, we’re seeing crypto finally making sense as a means of exchange.”

-John Collison, co-founder of Stripe

But the impact of stablecoins goes beyond corporate integrations. I’ve seen the need firsthand.

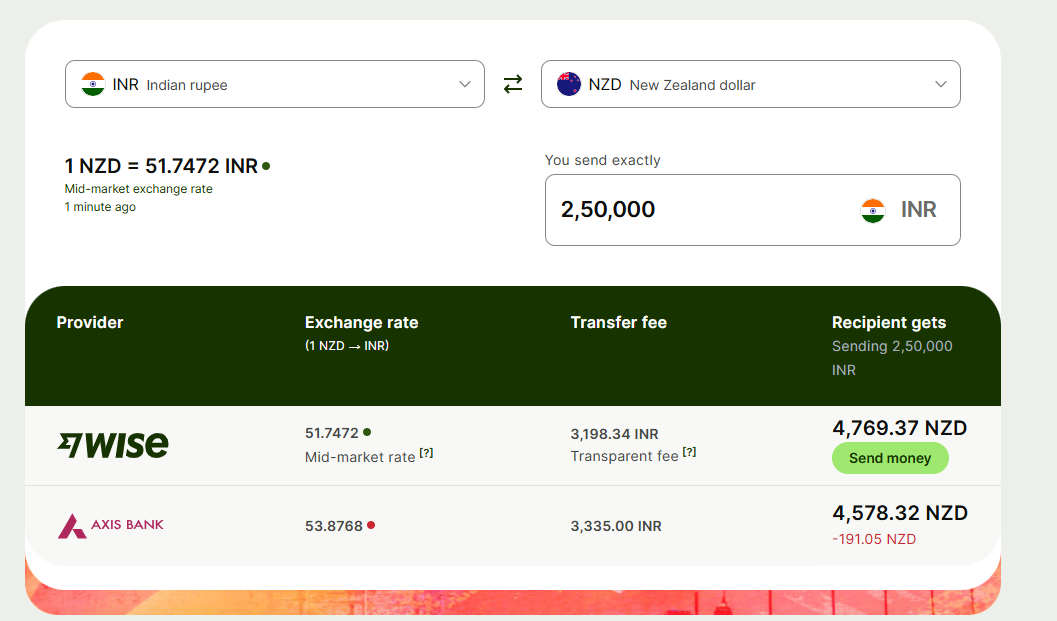

My brother is studying medicine in New Zealand. Every time my parents send him money, they lose money on fees, bad rates, and time. Transfers can take days, and banks happily pocket $50+ just for the privilege of moving our own money. Stablecoins on Solana, with integrations like Stripe in the future, could eliminate all of that friction. That’s not a crypto dream, it’s a necessity for families like mine.

According to KarbonCard, Every wire transfer is a toll road. FX margins, bank fees, SWIFT friction, what Stripe settles in seconds, banks drag out for days and charge you for the privilege.”

These aren’t edge cases. They’re everyday financial frictions that Solana stablecoins are finally making solvable at speed, and at scale.

Even Visa isn’t sitting still. In response to the Genius Act and broader regulatory momentum, Visa CEO Ryan McInerney emphasized that stablecoins aren’t a threat, they’re an opportunity. Visa has already embraced USDC and other stablecoins across its network, with real support for use cases like capital markets like crypto trading, emerging markets with unstable currencies or strict capital controls, and cross-border payments, including remittances and B2B transactions.

According to McInerney, the greatest growth opportunities for stablecoin adoption are likely outside the United States, where access to stable digital dollars can be especially valuable.

Mastercard, like Visa, isn’t treating stablecoins as a threat. It’s treating them as infrastructure.

Mastercard isn’t trying to compete with stablecoins, it’s absorbing them. While everyone was watching Visa and Stripe, Mastercard’s been quietly wiring stablecoins into the payments. We’re talking support for USDC, PYUSD, USDG, and FIUSD. Millions of wallets can already spend stablecoins at 150M+ merchants thanks to partnerships with the likes of MetaMask and Crypto.com.

Mastercard is turning stablecoins from an “alt payment method” into just… payments.

This isn’t some PR play. They're pushing real infrastructure: Crypto Credential, stablecoin settlement, even programmable B2B payments through the Multi-Token Network. This is traditional finance’s final form: not fighting crypto, not hyping it, just folding it in, with baking of fraud protection and compliance.

So while Solana isn’t mentioned directly (yet), let’s be honest: if Mastercard’s betting on fast, low-cost stablecoin rails, Solana’s not going to stay off their radar for long. They're not building for speculation, they're building for scale. And that’s exactly where Solana fits.

And it’s not just card networks playing catch-up. Commerce platforms are getting in too, where the stablecoin use case becomes brutally obvious.

Shopify didn’t build a crypto wallet. It didn’t issue a coin. It just did the smart thing: it plugged stablecoins into payments, right where it matters. Through a partnership with Coinbase and Stripe, Shopify merchants can now accept USDC over Base without touching any wallets, integrating new gateways, or worrying about crypto complexity. Customers pay in stablecoins, merchants get paid in dollars. No exchange fees. No delays. No nonsense.

This isn’t a marketing stunt. It’s real infrastructure for global commerce. For small businesses, cross-border payments are a pain: slow settlement, FX margins, random charges, and compliance overhead. Shopify’s stablecoin checkout cuts through that with something credit cards have never offered, global payments that are instant, final, and borderless.

The fact that it runs over a crypto network is beside the point. What matters is this: a Shopify seller in Nigeria or Argentina can now get paid like they live next to Stripe’s HQ. That’s not “Web3 innovation”, that’s what payments should’ve looked like a decade ago.

If the first wave of stablecoin adoption was about plugging into existing rails, this next one is about building entirely new ones. Projects like Squads, KAST, and Perena aren’t just using stablecoins, they’re architected around them. These aren’t flashy DeFi toys or protocol experiments, they’re serious attempts to turn stablecoins into programmable money, financial coordination tools, and treasury infrastructure. This is the frontier where stablecoins stop being a feature and become the foundation.

Native Stablecoin-Focused Products

Squads

Squads isn’t a wallet, it’s command central for on-chain teams.

It turns stablecoins into programmable capital and Solana into a serious operating system for crypto organizations. At its core, Squads offers multisig smart wallets built specifically for developers and teams on Solana and the SVM. It’s how crypto teams manage treasuries, control upgrade authority, stake funds, launch tokens, and collaborate securely without ever touching the CLI.

VC funds, validator keys, tokens, program upgrades, they all flow through a shared vault, with full auditability and granular controls. It’s infrastructure that actually respects the coordination chaos of crypto teams. And it’s not vaporware: everyone from MarginFi to Drift to Jito already uses it.

If stablecoins are financial building blocks, Squads is the command deck that makes them move.

Teams are now using stablecoins not just to store value but to operate with it: think salaries, grants, vesting schedules, validator rewards, contributor payments, all governed via transparent, multi-signature flows. Squads turns stablecoins from passive assets into programmable capital.

DAO payroll

Contributors get paid in USDC via pre-approved multisig flows. No missed invoices. No manual transfers. No rogue spending.Token vesting

Treasury managers lock stables or token reserves into time-bound multisigs, ensuring no one walks away with the bag.Operational budgets

Projects like Drift and Kamino allocate quarterly budgets to sub-teams via Squads, everything governed by on-chain approvals.Validator rewards

Stake SOL, manage validator income, and disburse incentives, all handled from a single interface that doesn’t require a developer.

KAST

If stablecoins are money, where’s the card?

KAST is a stablecoin-native financial platform built around global usability. It let users to spend stablecoins like USDC, USDT, and USDe through virtual and physical crypto cards at over 100 million merchants and ATMs worldwide. The platform is closely integrated with Solana, offering Solana-based cards and support for on-chain transactions. Beyond payments, KAST also supports on-chain savings and earnings, positioning itself as a complete financial stack for users who want to operate entirely in stablecoins. Its goal is to replace traditional fiat tools with blockchain-native alternatives that are fast, borderless, and accessible.

Perena

At a time when most liquidity protocols are still patching together fragmented pools, Perena is doing something Solana desperately needs: building a unified, scalable backend for stablecoin liquidity, starting with its Numéraire AMM. Rather than chasing volume with gimmicks, Perena uses a hub-and-spoke model that concentrates liquidity where it matters, around the peg, and extends it outward to partner stablecoins via bounded, composable pools.

The result is USD* (USD Star), a stablecoin-backed LP token representing pooled USDC, USDT, and PYUSD. But this isn’t another wrapped token, USD* is a yield-bearing, composable asset at the center of Perena’s ecosystem. It connects capital-efficient core pools with isolated growth pools, allowing new stablecoin issuers to tap into shared liquidity without importing risk. It’s how Solana finally gets a shared backend for stablecoin swaps, issuance, and yield, all in one.

This isn’t an experiment. Perena has already processed $2.1B+ in stablecoin volume, and it’s just getting started. The team includes veterans from the Solana Foundation and Jump, with backing from Anatoly and Raj. If Solana is going to own the stablecoin layer, it needs something like this under the hood: deep liquidity, capital efficiency, and a protocol that actually understands the economics of stability. Perena gets it. And they’re building like it.

All the products above depend on one thing: stablecoins that actually work. Not just in theory or in trading pairs, but at scale, under pressure, and across jurisdictions. That’s where issuers come in. While USDC and USDT still dominate, they weren’t built for the world we’re heading into. A new crop of issuers like, PYUSD, USDG, USDe, sUSD and others are stepping in with fresh models, new distribution paths, and regulatory-first design. This next section looks at the players reshaping the base layer itself.

Emerging Stablecoin Issuers

With USDC and USDT already dominating the stablecoin market, the obvious question is: why launch another one?

USDC and USDT already dominate the market together, they’ve captured nearly every major integration, protocol, and payment rail. On the surface, launching a new stablecoin seems redundant. But peel back the hype, and the reasons are actually practical, even obvious.

Some ecosystems don’t want to be dependent on someone else’s coin. Some need compliance tailored to their local laws. Others are building stablecoins as tools for specific use cases like salary payments, on-chain savings, or RWA settlement. And for some, it’s just about trust. Tether’s always had reserve questions. Circle depends on US banking rails. If you’re building a global protocol, you can’t afford that kind of fragility.

Suggested Read: What Is PayPal Stablecoin, And Can It Compete With USDT And USDC? - B2Binpay

So now we’re seeing a new wave of stablecoin issuers, exchanges, fintechs, even infrastructure protocols, all launching their own version of a digital dollar. Some of them are just branding exercises. But a few are actually pushing the category forward.

PYUSD

Startups aren’t the only ones chasing stablecoin innovation, PayPal, one of the largest fintech companies in the world, is betting that the future of money is programmable. Their launch of PYUSD is issued by Paxos and regulated by the NYDFS. Stablecoins are going mainstream, and the incumbents want in. Unlike USDC or USDT, PYUSD isn’t built for DeFi yield farms or on-chain casinos. It’s designed for Venmo, PayPal checkout, peer-to-peer payments, and eventually settlement across Mastercard rails. And while it runs on Ethereum, the blockchain is deliberately invisible to the average user because PayPal doesn’t want you to “use crypto,” it wants you to send digital dollars without friction.

That’s the strategy. Forget Metamask. Forget seed phrases. PayPal is going full Apple-mode: abstract the crypto, keep the UX. But here’s the real question: will people actually care? PYUSD hasn’t exactly lit up the charts on-chain, and crypto-native users mostly ignore it.

PYUSD hasn’t exactly lit up the charts on-chain, and crypto-native users mostly ignore it.

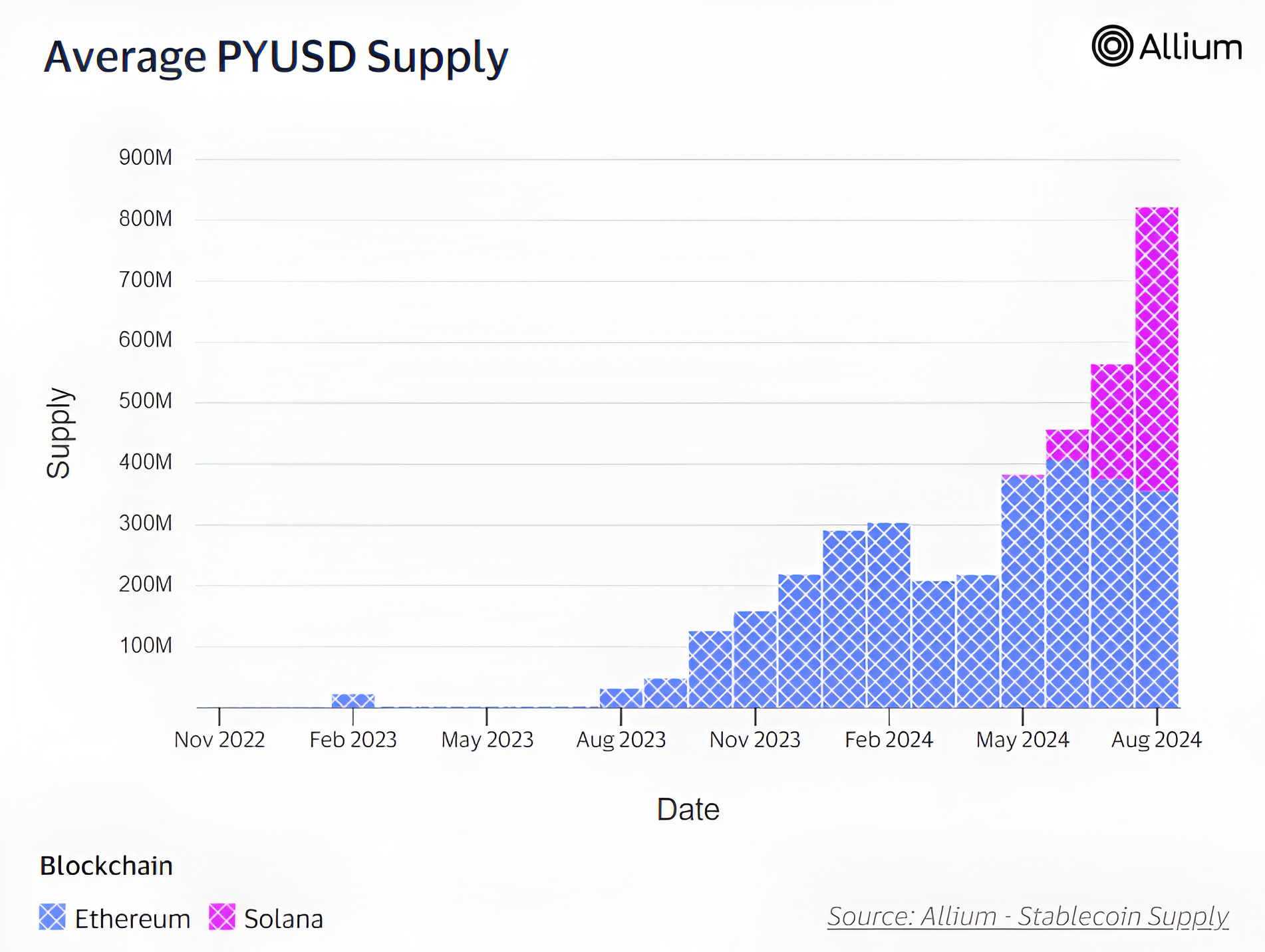

But the supply tells a different story. Since launch, PYUSD’s average monthly supply has grown steadily on Ethereum and since May 2024, Solana has begun capturing a significant share. In just a few months, over 300 million PYUSD is now circulating on Solana, pushing total supply past 800 million.

This quiet but accelerating footprint reflects PYUSD’s real target: not traders, but mainstream users. Solana’s low-cost, fast-settlement environment makes it ideal for PayPal’s ambitions around everyday commerce, remittances, P2P, and checkout flows. The blockchain may be invisible, but the infrastructure choice isn’t accidental.

But maybe that’s the point. PYUSD isn’t fighting for mindshare on DeFi dashboards, it’s coming for the next 50 million users who’ve never touched a wallet and never will. That might be boring to crypto purists. But boring, at scale, is how payments win.

USDG

USDG isn’t flashy, but it’s designed to be boring enough to get regulators and banks comfortable. It’s built by Paxos, backed by global heavyweights like Kraken, Robinhood, Anchorage, and Mastercard via the Global Dollar Network . Issued under Singapore’s upcoming stablecoin framework and audited monthly, USDG is all about trust and transparency, “fully backed by cash and cash equivalents”.

What sets it apart from USDC/USDT isn’t better tech, it’s the distribution strategy. Kraken already supports a rewards program offering up to 4% APR for holding USDG, signaling this is meant to sit, settle, and earn, not trade or pump. And it’s already live on Ethereum and Solana , which means real on-chain utility, not just boardroom lip service.

But make no mistake, it’s not built for DeFi. This is middleware. Banks, fintechs, exchanges, they’ll mint, settle, and tuck this under existing systems. The average user won’t know or care. That’s the point. In a world of hype and speculation, USDG is quietly slipping into the plumbing part of the quiet backbone that powers everything else.

FDUSD

First Digital USD is a Hong Kong–issued, fiat‑backed stablecoin launched in June 2023 by First Digital Labs (FD121) under Hong Kong’s Trust Ordinance. It’s fully backed 1:1 with U.S. dollars and short-term U.S. Treasury bills held in segregated accounts, audited monthly since July 2023 and as of October 2024, it had $2.552B in reserves supporting $2.539B in circulation.

However, it wasn’t all smooth sailing. In April 2025, Justin Sun, founder of Tron, publicly accused First Digital of insolvency, briefly knocking FDUSD down to $0.87. The coin has since recovered after FD refuted the claims, confirmed its reserves (exceeding supply), and Binance reaffirmed the peg with its own audit. Still, Binance controls around 94% of FDUSD’s supply, putting a massive concentration risk in the market.

FDUSD’s supply has fluctuated, growing to over $2.5B, then sliding back towards $1.9B after Binance ended trading incentives, even as it remains a top‑tier fiat-backed coin.

USDP

Pax Dollar (USDP), formerly Paxos Standard is the oft-overlooked, quiet, regulated engineer in the room. It launched in September 2018, rebranded in 2021, and expanded onto Solana and Ethereum in early 2024. It’s not flashy, but that’s exactly the point.

It is regulated by NYDFS and backed 100% by cash and cash equivalents. Unlike volatility-prone rivals, USDP offers real consumer protections: segregated reserves, monthly audits, redemption guarantees, classic compliance baked in.

But here’s what catches my attention, Paxos didn’t just mint another token, they built a pay-ins API platform with Stripe integration, supporting USDP alongside USDC and PYUSD. In other words, Paxos is quietly slipping stablecoins into existing financial plumbing, Stripe merchants can accept crypto without feeling like they're “on-chain.” That's middleware with teeth.

Critically though, USDP still lags in adoption. Market cap sits in the low hundreds of millions, far behind USDC or USDT. That niche position is a two-edged sword, it’s trusted, but not dominant.

sUSD

sUSD is the kind of stablecoin the ecosystem actually needs. It is built on Solana, backed by U.S. Treasuries, and paying real yield without the hype. Launched by Solayer and OpenEden, it’s one of the first on-chain dollar tokens designed to passively grow in your wallet at ~4–5% APY thanks to tokenized T‑Bills. That means you get a genuine cash equivalent you can spend, stake, or swap, and it earns yield automatically. Anyone can mint sUSD with as little as $5 on Solana, and the yield is credited in real time.

It is built for utility. By simplifying both spendability and yield, Solayer is placing money-management into users’ wallets, not just DeFi dashboards. But its $11 M TVL and niche positioning show it’s still early, this is an infrastructure experiment, not mainstream money… yet. Still, the fact that someone finally built a yield-bearing digital dollar on Solana speaks volumes about where the ecosystem is headed and why the base layer matters.

And it’s not just crypto startups or fintech giants. The stablecoin wave is now creeping into the most traditional corners of commerce and finance. Fiserv is reportedly exploring stablecoin payment rails for merchants; JPMorgan is already piloting blockchain-based deposit tokens for corporate clients; Walmart filed patents hinting at a branded digital dollar; and Amazon is quietly experimenting with stablecoin integrations through AWS and select Prime markets.

These aren't just experiments, they're signals. Stablecoins are no longer fringe financial toys. They’re becoming the settlement layer for everything, from payroll to e-commerce. When the giants start building base-layer money primitives, you pay attention.

Regulations & Global Trends

New stablecoins are launching left and right, but it’s not just tech or liquidity that decides who wins. The real battleground is regulation. Whether you’re a fintech giant or a DeFi startup, your stablecoin is only as useful as the jurisdictions it can operate in. And as governments start laying down real frameworks, not tweets, not memos, the global stablecoin map is being redrawn. This next section looks at how regulation, licensing, and geopolitics are shaping the future of stablecoins, from Washington to Singapore to the Global South.

U.S. – GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins)

Congress didn’t just give a polite nod to stablecoins, it slammed them into the legal fast lane. The GENIUS Act, passed by the Senate 68–30 in June 2025, doesn’t dabble in vague regulation: it mandates stablecoins must be fully backed by cash or ultra-safe assets, with monthly audits, anti-money laundering controls, and legal protections for holders in bankruptcy. It carves out “payment stablecoins” as a new, regulated asset class, no longer commodities or securities. Critics say it’s too rigid, and could echo the failures of past liberal financial loopholes. But Tether’s leadership just dropped like a sack of bricks from $156 b liquidity when they refused to comply. Meanwhile Circle and PayPal are practically doing cartwheels, they’ve already checked every compliance box and are positioned to thrive. The GENIUS Act isn’t some hopeful proposal, it’s a legislative groundhog day, forcing a trillion-dollar question: adapt or vanish.

EU – MiCA (Markets in Crypto-Assets Regulation)

The EU’s MiCA framework, adopted in April 2023. It is the first comprehensive crypto law by a major economic bloc and it doesn’t mess around. It categorizes stablecoins into two buckets: e-money tokens (EMTs) like USDC (pegged to one fiat currency), and asset-referenced tokens (ARTs) like multi-collateral or commodity-backed coins. It mandates full 1:1 backing, monthly reserve audits, and issuer licensing across all 27 EU countries. And if you want to issue a "significant" stablecoin under MiCA? At least 60% of reserves must be held in European bank deposits or low-risk liquid assets, not ideal in a world where banks themselves are often the weak link.

Tether’s CEO didn’t hold back, calling this rule “potentially dangerous,” arguing that forcing stablecoins into overleveraged European banks could create the exact kind of systemic risk the law is trying to avoid. But the EU isn’t aiming for crypto-native use cases here, it’s designing stablecoins for regulated finance, corporate treasuries, and retail payments. Whether it helps or hinders remains to be seen. What’s clear is this: MiCA isn’t just about oversight, it’s about control. And it could become the gold standard, or the biggest regulatory bottleneck the crypto industry has faced yet.

Singapore & Hong Kong

Singapore used to be the sandbox; now it’s the crackdown. As of June 30, 2025, any Singapore-based firm offering crypto services abroad must hold a license under the Financial Services and Markets Act (FSMA), no excuses, no extensions. Retail protections are aggressive: banned credit-card crypto purchases, no promotions, mandatory risk assessments, plus ID checks on transactions over SGD 1,500 (“Travel Rule”). Even DeFi frontends and non-custodial wallets can fall under these rules if they serve users or generate revenue in the region.

Across the water, Hong Kong just threw down its own guardian guardrails. On August 1, 2025, the HKMA will begin issuing licenses to fiat-referenced stablecoin issuers under the new Stablecoins Ordinance. Reserve requirements are tough, a full 100% backing in cash or government bonds is mandatory. Sandbox participants already include heavyweights like Standard Chartered, Animoca, and Ant Group. The message is clear: Hong Kong wants stablecoins, but only under full, corporate supervision.

These aren’t incremental updates, they’re signals. Singapore is sealing loopholes, removing “light touch” cover for global operators. Hong Kong is leaning into tokenization, but only with tight control.

The takeaway: Asia’s crypto gateway is closing for the unlicensed and opening only for the compliant.

Global – BIS Warning

While new stablecoins continue to launch and regulators carve out jurisdictional frameworks, not everyone is optimistic. In June 2025, the Bank for International Settlements (BIS) often described as the central bank for central banks issued its starkest warning yet against stablecoins, calling them “a risk to financial stability and monetary sovereignty.”

The BIS criticized their lack of true settlement finality, transparency over reserves, and potential for triggering capital flight in emerging economies. Tether’s recent EU exit over MiCA compliance only amplified the core issue: in the BIS’s view, private stablecoins remain structurally flawed substitutes for sovereign money. Instead, the BIS is calling for bold action toward tokenized, programmable central bank money suggesting that the future of stable finance may lie with digital public infrastructure, not private coins.

Across the board, regulators are coalescing around the idea that stablecoins should behave like digital cash, fully backed, transparent, and compliant. But how that’s enforced varies sharply. The US is creating new categories, the EU is imposing structural limits, and the BIS would rather they didn’t exist.

The common thread? Permissionless doesn’t mean lawless anymore. The age of crypto regulatory arbitrage is ending and the compliant players are the ones being handed the keys to the future.

Opportunities: What Comes Next

Stablecoins on Solana have proven themselves across payroll, remittances, and commerce. But we’re still scratching the surface.

Cross-Border Invoicing for Freelancers

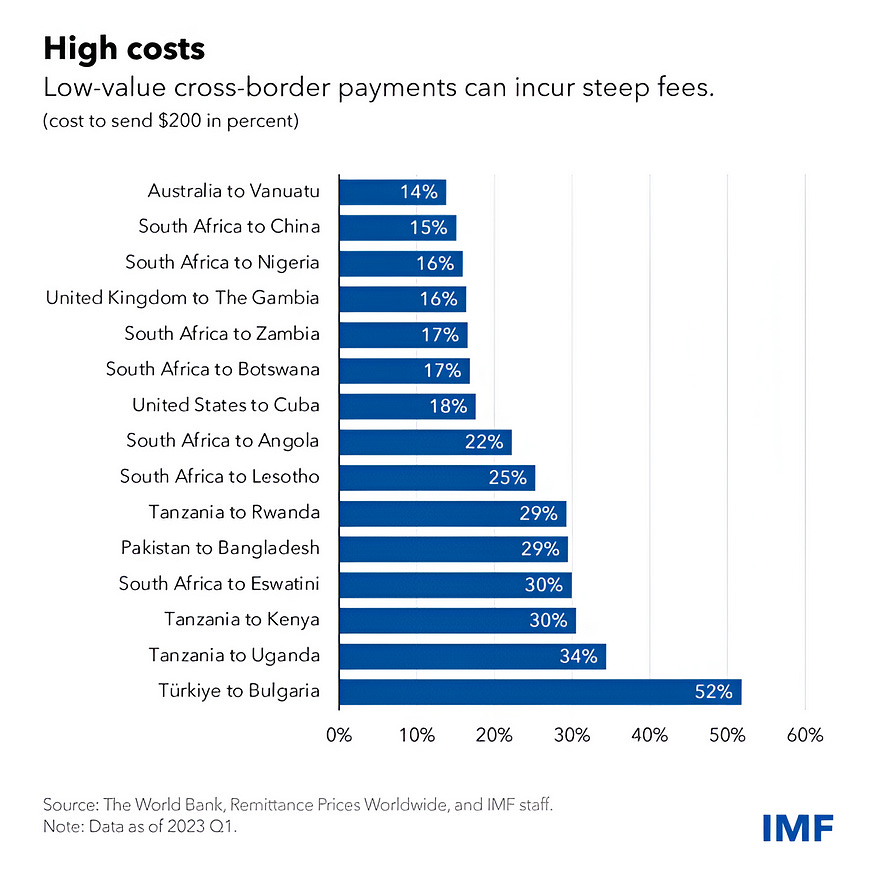

Freelancers today face a broken payments system. If you’re based in India, Nigeria, Argentina, or the Philippines and working for global clients, your payment can take days or weeks. Platforms like PayPal eat 4–8% in fees, banks layer on FX spreads, and wire transfers often fail or get held. There’s no visibility, no instant settlement, and no guarantee of fair conversion rates.

A lightweight invoicing app can solve this problem, an app that lets freelancers create invoices in local currency (e.g., INR) using a web app. The client pays in fiat via Stripe, which handles KYC, compliance, and off-ramp.

The fiat gets auto-converted to USDC, settled instantly on Solana, and credited to the freelancer’s wallet.

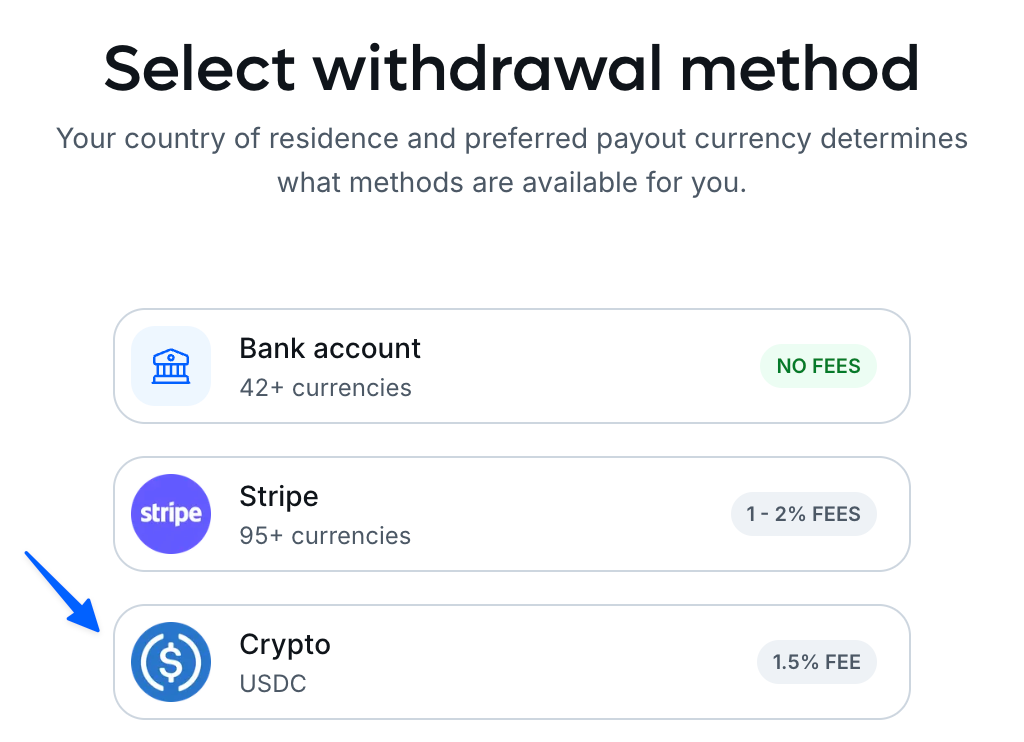

Freelancers can hold the USDC, cash out via a local exchange, or route it directly to a linked debit card (via platforms like KAST) or off-ramp provider like Transak.

Payments settle in seconds.

Fees drop from 5–10% to under 1%.

No more wondering if the payment went through.

The app can offer integrated yield via sUSD or similar instruments, turning idle balances into passive earnings until withdrawal.

On-Chain Dividend Distribution

For tokenized equity and RWA platforms, stablecoins can power frictionless dividend and coupon payments with transparent audit trails and programmable compliance.

The promise of tokenized assets, equity, bonds, real estate isn’t just better trading. It’s better ownership infrastructure. But the moment these assets generate yield (dividends, interest, rent), things get messy.

In TradFi, dividend distribution is a nightmare of intermediaries. Custodians batch payments, banks clip fees, FX spreads apply if you're abroad, and there’s no real-time traceability. Worst of all, global investors often get penalized simply for being in the "wrong" country, with inconsistent tax treatment and friction-heavy settlement processes.

An on-chain dividend engine fixes all of this.

Tokenized securities track ownership on-chain, whether equity in a startup, fractionalized real estate, or a yield-bearing bond.

At payout time, the protocol calculates pro rata entitlement and distributes stablecoins (USDC, sUSD, USDG) directly to wallet addresses, no intermediaries, no custodians.

Settlement is instant, and every transaction is verifiable on-chain, no PDFs, no third-party batch reports.

Whether a property in London is tokenized for investors in Brazil or a startup in India raises from DAO members worldwide, stablecoins on Solana let it all work without a mess of wires and legal headaches.

This isn’t theory, it’s inevitable. As tokenized public and private markets grow, dividend distribution becomes not just a feature, but a core primitive. And stablecoins on fast, low-cost chains like Solana can make it viable.

Consumer-Grade Interest Accounts

Stablecoins that generate yield, backed by short-term U.S. Treasuries, can enable compliant, yield-bearing savings tools for underserved global markets without relying on centralized finance custodians.

In many regions across LATAM, Southeast Asia, and Africa, users face limited access to stable savings products. Local banks often offer poor interest rates, high inflation erodes value, and USD access is restricted or expensive. Meanwhile, most crypto yield products rely on CeFi platforms that come with counterparty risk and lack regulatory clarity.

A new class of interest-bearing stablecoins changes this.

Built on open protocols like Solayer on Solana, these stablecoins are backed 1:1 by U.S. Treasury bills and accrue real yield directly in the user’s wallet. There are no staking steps, no lockups, and no need for CeFi platforms to manage the funds.

This creates the foundation for consumer-grade mobile apps that offer:

Real-time interest accrual, automatically reflected in wallet balances.

Dollar-denominated savings, accessible globally via stablecoin rails.

Low minimums, often as little as $5 to get started.

Non-custodial access, where users retain full control of funds.

Built-in compliance filters, to support KYC/AML and regional regulatory rules.

For users, this would feel like a savings account, deposit money, earn passive yield, and withdraw anytime. For providers, it’s a scalable fintech model built on DeFi infrastructure with regulatory flexibility and composability.

This kind of product is especially valuable in high-inflation markets or places with capital controls, where even 4–5% APY on stable dollar value can make difference.

The combination of stable, yield-generating assets with a clean user interface and local on/off ramps could become a gateway product for onboarding millions into on-chain finance, without exposing them to the risk, complexity, or volatility of traditional crypto platforms.

Closing Thoughts

Stablecoins have quietly become the most functional and widely used product in crypto. Not because they’re flashy, but because they solve real problems, payments, payroll, remittances, settlements.

This isn’t theoretical. It’s happening in production, at scale, with real users and real infrastructure. Solana’s speed, cost-efficiency, and ecosystem maturity have made it the most viable platform for stablecoin adoption today. What was once an afterthought is now a structural pillar of the network.

The future of money isn’t about replacing fiat, it’s about making it programmable, accessible, and borderless. Stablecoins are delivering that. Solana is where they’re being deployed.

References

Solana’s Stablecoin Landscape - Helius

What are stablecoins, and how are they regulated? - Brookings

Visa and Mastercard - Forbes

What is Squads? - Blog by Squads

Perena: The unified stablecoin infrastructure - Mitosis University

PYUSD - Solana

Stablecoins 101 for Payments Professionals - Fireblocks

Stablecoin Development on Solana - Solulab [Solid Analysis Worth Reading]

Stablecoin Regulation 2025 - Phemex

What You Need To Know About Incoming Stablecoin Legislation - Arnold & Porter

Robust and Sustainable Development of Stablecoins - Hong Kong Monetary Authority

The Genius Act: U.S. Stablecoin Framework Proposal - Congress.gov

(All other sources are cited in-line with hyperlinks.)

Well done, Vivek

Nicely done bro 👏